On April 30, 2020, the Federal Reserve announced the expansion of the scope and eligibility for the Main Street Lending Program (MSLP) and clarified key aspects of the original term sheets released April 9, 2020. The MSLP was created to help credit flow to small and medium-sized businesses that were in sound financial condition before the pandemic. A start date of the program will be announced soon. The key changes made through the revised term sheets include:

- Creating a third loan option, with increased risk-sharing by lenders for borrowers with greater leverage;

- Lowering the minimum size for certain loans to $500,000; and

- Expanding the pool of businesses eligible to borrow.

Eligible borrowers should contact their existing financial institution for more information on the application process.

Key Details of the MSLP

- Loan facilities available under the program:

- Newly originated loans

- Main Street New Loan Facility (MSNLF)

- Main Street Priority Loan Facility (MSPLF)

- Expansion of existing loans

- Main Street Expanded Loan Facility (MSELF)

- Lender retention and risk of loss of loans

- MSNLF - 5% retained by lender; 95% sold to the MSLP Special Purpose Vehicle (SPV) and the risk will be shared between the lender and the SPV on a pari passu basis

- MSELF - 15% retained by lender; 85% sold to the SPV and the risk will be shared between the lender and the SPV on a pari passu basis

- MSPLF - 5% retained by lender; 95% sold to the SPV and the risk will be shared between the lender and the SPV on a pari passu basis

- Available funds

- The SPV is authorized to purchase up to $600 billion in MSLP loan participations until September 30, 2020.

- Interaction with CARES Act programs

- Businesses receiving loans through the Paycheck Protection Program (PPP) under the CARES Act may also participate in the MSLP. Unlike the PPP, no portion of MSLP loans are forgivable.

- Key Certification

- Borrowers must commit to make “commercially reasonable efforts” to maintain payroll and retain workers through the term of the loan. The Federal Reserve has defined “commercially reasonable efforts” as good faith efforts to maintain payroll and retain employees, in light of its capacities, the economic environment, its available resources, and the business need for labor. Businesses that have already laid-off or furloughed workers due to COVID-19 are still eligible for the MSLP.

- Underwriting

- The key underwriting metric required by the MSLP is EBITDA. For organizations generally not evaluated on the basis of EBITDA, including nonprofits and asset-based businesses, the Federal Reserve and Treasury Department will evaluate the feasibility of adjusting borrower eligibility criteria and loan eligibility metrics.

- Newly originated loans

Borrower Eligibility Requirements[1]

- Borrowers must be organized in the United States or under the laws of the United States, with significant operations in and a majority of employees located in the United States. Borrowers must have been in good financial standing before the COVID-19 crisis and must need financing resulting from exigent circumstances presented by the pandemic. The term “good financial standing” has not been defined.

- Borrowers must have 15,000 or fewer employees or revenues $5 billion or less. Employees and revenues of affiliated businesses must be aggregated in the determination of the number of employees and revenues of the business.

- Businesses should use the average number of persons employed for each pay period over the 12 months prior to the origination or expansion of the MSLP loan. In determining the number of persons employed for each pay period, the business should count each full-time, part-time, seasonal or otherwise employed persons, excluding volunteers and independent contractors.

- A business may use its (and its affiliates') annual revenue per its 2019 GAAP audited financial statements or use its annual receipts for the fiscal year 2019 as reported to the IRS. If 2019 statements are not prepared, the borrower should use its most recent audited financial statement or annual receipts.

- Borrowers can only participate in one of the facilities created under the MSLP and may not also participate in the Primary Market Corporate Credit Facility.

- Borrowers must meet the underwriting standards of the lender; therefore, borrowers meeting the minimum requirements for the MSLP will not automatically qualify for a loan and may not receive the maximum allowable loan amount.

Exhibit A:

Intended Borrowers for Each of the Main Street Lending Programs

As the availability of credit has contracted for many small and medium-sized companies as a result of the pandemic, the intent of the Main Street Lending Program (MSLP) is to ensure companies have access to financing. The loans are intended as bridge loans to assist borrowers in maintaining their operations and payroll until conditions normalize. Though the three MSLP programs have the same eligibility criteria, they differ in how they interact with the borrower’s existing outstanding debt, including the debt incurred prior to the pandemic.

Main Street New Loan Facility (MSNLF) –

This facility is generally intended for companies that did not use debt as a part of their operations prior to the pandemic. Companies that were not previously using debt will likely not need as much funding in order to continue operations through the pandemic. As a result, the funds available are limited to 4x adjusted EBITDA. Companies needing funding in excess of 4x EBITDA may have access to the larger loans through the MSPLF discussed below. There is a key difference in the repayment terms between the MSNLF and MSPLF. The total amount to be repaid by the company will be lower under the MSNLF as larger principal payments are required in years 1 and 2 resulting in less interest accruing over the life of the loan. However, consideration should also be given to the expected recovery period as the MSNLF requires a principal payment of 33% at the end of year 2 while the MSPLF only requires a principal payment of 15%.

Companies that have existing debt with lenders other than the eligible lender for this loan will likely be precluded from using this facility as the borrower must certify that payments will not be made on the existing debt that ranks pari passu to this loan until this loan is fully paid.

Main Street Priority Lending Facility (MSPLF) –

This facility is generally intended for small and mid-size companies that are currently using debt as part of their capital structure. Because the borrower must certify that that payments will not be made on the existing debt that ranks pari passu to this loan until this loan is fully paid, the borrower may refinance its loans with other lenders into this loan facility. As the company has existing debt, the maximum funds that may be borrowed is greater for the MSPLF than the MSNLF.

Main Street Expanded Loan Facility (MSELF) –

This facility is generally intended for the larger companies that fall within the eligibility criteria and have existing debt with the eligible lender. The minimum amount of additional borrowings under this facility is $10 million. To qualify for this facility, borrowers must already have approximately $29 million in existing outstanding and undrawn available debt.

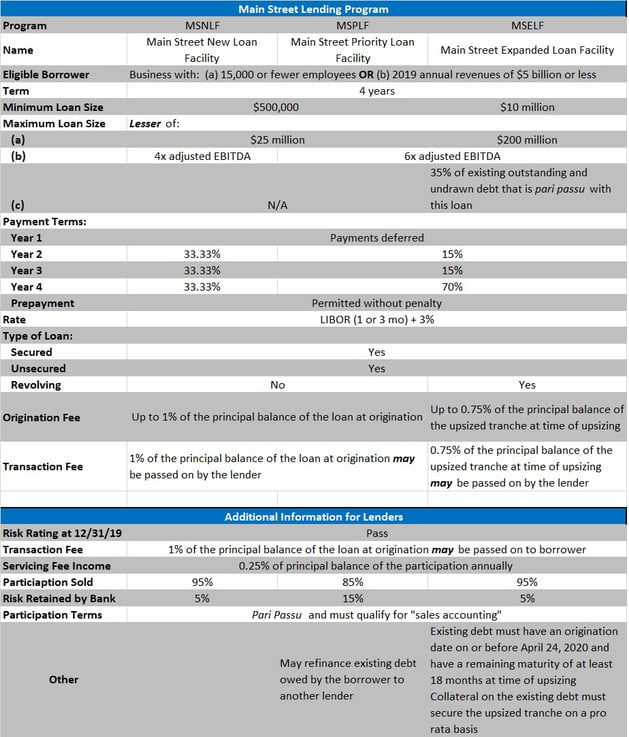

Loan Terms[2]

- Maturity

- 4-years

- Interest Rate

- Adjustable rates of LIBOR (1 or 3 month) plus 300 basis points. Based on the May 6, 2020 1-month LIBOR Rate (0.2216%), the interest rate would be 3.22%.

- Payments

- Principal and interest payments are deferred for one year with unpaid interest capitalized.

- No prepayment penalty.

- Loan size and Loan Amortization

Exhibit B:

[1] See Exhibit A for information on the intended borrowers for each MSLP credit facility.

[2] See Exhibit B for a summary table of the loan terms applicable to each MSLP credit facility.

HoganTaylor's Advisory PracticeIf you have any questions about this content, or if you would like more information about HoganTaylor's Advisory practice, please contact Robert Wagner, Advisory Partner, at rwagner@hogantaylor.com. More information is also available on the Advisory practice page of this website. INFORMATIONAL PURPOSE ONLY. This content is for informational purposes only. This content does not constitute professional advice and should not be relied upon by you or any third party, including to operate or promote your business, secure financing or capital in any form, obtain any regulatory or governmental approvals, or otherwise be used in connection with procuring services or other benefits from any entity. Before making any decision or taking any action, you should consult with professional advisors. |

Get Updates