UPDATE: This article has been updated to reflect the legislation’s passage into law on December 27, 2020

By Clay Glasgow, CPA, ABV, CFF, CFE, Advisory Partner and Leah McLain, CPA, Advisory Practice Consulting Manager

For more information on the tax implications of this legislation, read Pending Presidential Signature, Congress Has Enacted Historic Pandemic Relief Bill… Again

On December 27, the Consolidated Appropriations Act, 2021, a $2.3 trillion spending bill that includes a $900 billion stimulus package intended to provide additional financial relief to individuals and businesses impacted by the COVID-19 pandemic, was signed into law by the President.

The Act contains follow-on provisions to the CARES Act and the Paycheck Protection Program enacted in the Spring of 2020. This article highlights key provisions of Division N, Title III, Continuing the Paycheck Protection Program and Other Small Business Support related to the forgiveness of existing PPP loans and PPP second draw loans.

Updates to Paycheck Protection Program Loan Forgiveness

Key changes to PPP loan forgiveness are summarized below. These changes are effective as if they were included in the CARES Act originally and are thus applicable to both existing and new second draw loans (except in the case of loans that were already forgiven at the time the legislation is enacted, unless otherwise noted):

- Taxability: clarification has been provided regarding taxability of PPP loan forgiveness. Loan forgiveness is excluded from taxable income, and qualifying business expenses paid using PPP loan proceeds are indeed deductible, even if the loan is forgiven.

- Additional eligible expenses: in addition to payroll costs, mortgage interest, rent, and utilities; eligible expenses will now include covered operations expenditures, covered property damage costs, covered supplier costs, and covered worker protection expenditures.

- Simplified forgiveness for loans up to $150,000: for loans under $150,000, borrowers will have a simplified forgiveness application process consisting of signing and submitting a certification to the lender which: 1) is no more than 1 page in length; 2) indicates the number of employees the borrower was able to retain because of the loan, the estimated amount of the loan spent on payroll costs, and the total loan value; and 3) attests that the borrower has accurately provided the required certification, has complied with all the requirements of the PPP loan program, and retains records to prove compliance with requirements for 3-4 years (depending on record type).

- Audits: within 45 days after enactment, the SBA must submit to the Senate and House of Representatives a plan for conducting reviews and audits of covered loans of more than $150,000 and the metrics that the SBA shall use to determine which loans to audit. Within 30 days after submitting the plan, and each month thereafter, the SBA must submit a report on the status of their forgiveness review and audit activities.

- Expanded definition of benefits as part of payroll costs: in addition to group health care benefits, payroll costs will now include group life, disability, vision, or dental insurance costs.

- Repeal of EIDL Advance Deduction: previously, borrowers who received a PPP loan as well as an EIDL advance had to deduct the amount of their EIDL advance from the amount of their PPP loan forgiveness. This EIDL advance deduction is now repealed. The SBA will establish a process for borrowers who have already received PPP loan forgiveness and who had an EIDL advance deducted from their loan forgiveness amount to be made whole.

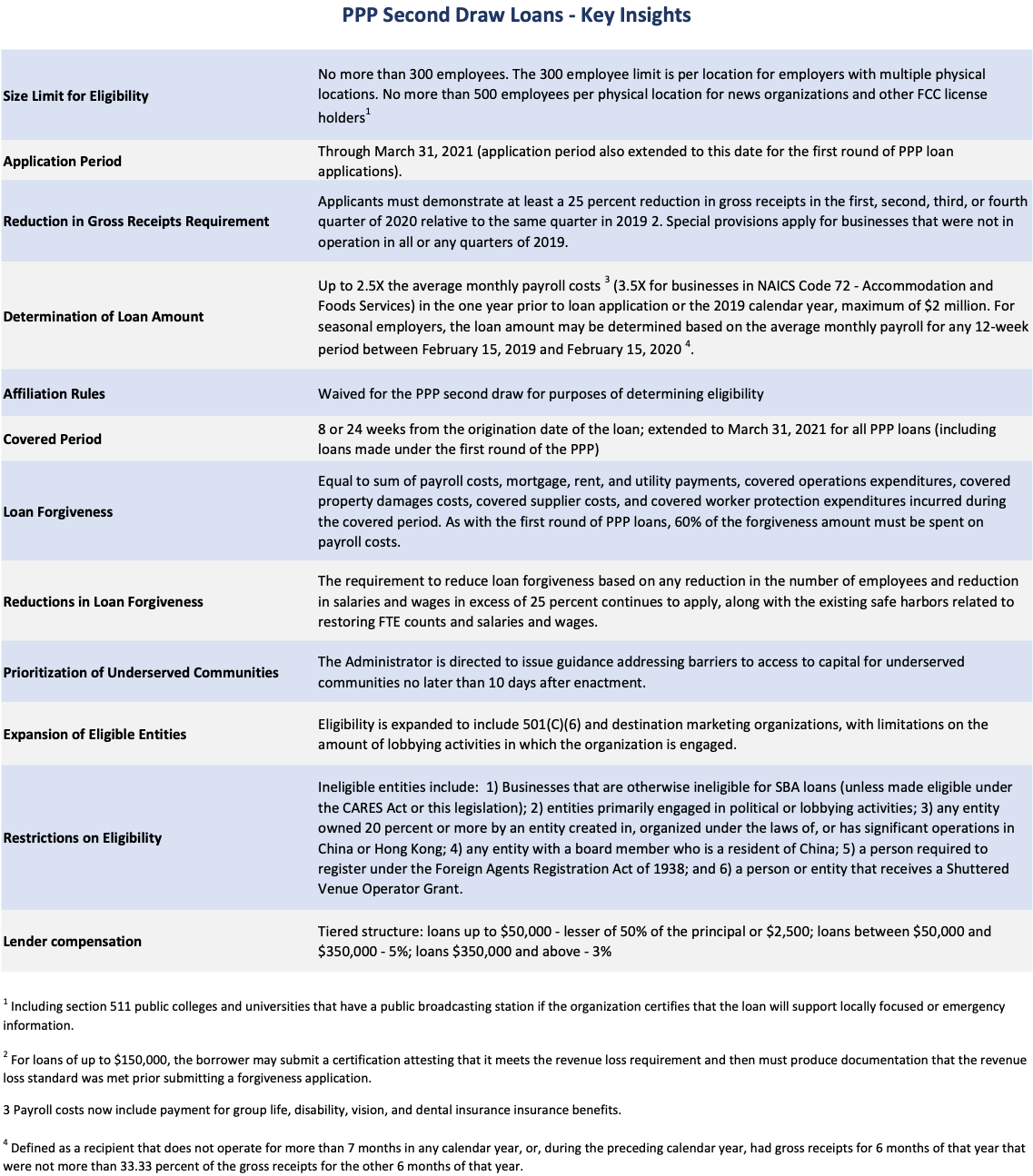

Paycheck Protection Program Second Draw Loans

A second PPP loan, referred to as a “PPP second draw,” will be available to certain eligible businesses. The PPP second draw is designed to provide relief to smaller businesses that have been more significantly hurt by the pandemic as compared to the first round of PPP loans. The following table outlines key provisions related to the PPP second draw.

Further details on the changes in PPP loan forgiveness and the PPP second draw loans can be found in the House of Representatives’ summary of the provisions of the Coronavirus Response and Relief Supplemental Appropriations Act can be found here.)

HoganTaylor will continue to provide guidance and valuable insights as more information becomes known about the PPP and other financial relief programs.

HOW HOGANTAYLOR CAN HELPHoganTaylor has assembled a team to monitor developments in financial assistance available to businesses hurt by the COVID-19 pandemic. We have been working to understand the legislation and guidance being issued to support the various programs available to affected businesses so that we can provide relevant and timely advice to our clients. As information becomes available, we will continue to recommend specific actions to take to effectively access these programs. If you need assistance in evaluating your company’s PPP loan certifications or in drafting documentation to support the evaluation and conclusions surrounding your certifications, please contact a HoganTaylor advisor at SBALoans@hogantaylor.com. INFORMATIONAL PURPOSE ONLY. This content is for informational purposes only. This content does not constitute professional advice and should not be relied upon by you or any third party, including to operate or promote your business, secure financing or capital in any form, obtain any regulatory or governmental approvals, or otherwise be used in connection with procuring services or other benefits from any entity. Before making any decision or taking any action, you should consult with professional advisors. |

Get Updates